Explore the intricacies of capital gain under the Income Tax Act in India. Learn about its implications, exemptions, and calculations. Get expert insights and answers to frequently asked questions.

Blog post description.

INCOME TAX

The Indian Income Tax Act outlines various provisions and regulations related to taxes, and one critical aspect is capital gains. This article will delve into the details of capital gain under the Income Tax Act in India. Whether you're an investor, a taxpayer, or someone looking to understand the tax implications of capital gains, this guide will provide you with comprehensive insights and answers.

Introduction

Capital gains refer to the profits earned from the sale of assets such as real estate, stocks, mutual funds, or valuable items. These gains are subject to taxation under the Income Tax Act in India. Understanding the nuances of capital gains is essential to ensure proper compliance with tax regulations and to make informed financial decisions.

Capital Gain under Income Tax Act India: Exploring the Basics

Capital gain under the Income Tax Act in India is categorized into two types: short-term capital gain (STCG) and long-term capital gain (LTCG). The distinction between these two is based on the holding period of the asset. If an asset is held for 36 months or less before being sold, the resulting gain is considered STCG. On the other hand, if the holding period exceeds 36 months, the gain is categorized as LTCG.

Capital Gain Holding period = Capital Gain

1) Shares /Security Less than 12 Months = Short Term (STCG) More than 12 Months = Long Term (LTCG)

2) Immovable Property/ Unlisted shares Less than 24 Months = Short Term (STCG) More than 24 Months = Long Term (LTCG)

Understanding the Calculation of Capital Gain

Calculating capital gains involves several factors, including the cost of acquisition, cost of improvement, and sale price. The formula for calculating capital gain is as follows:

Capital Gain = Sale Price - (Cost of Acquisition + Cost of Improvement + Other Related Costs)

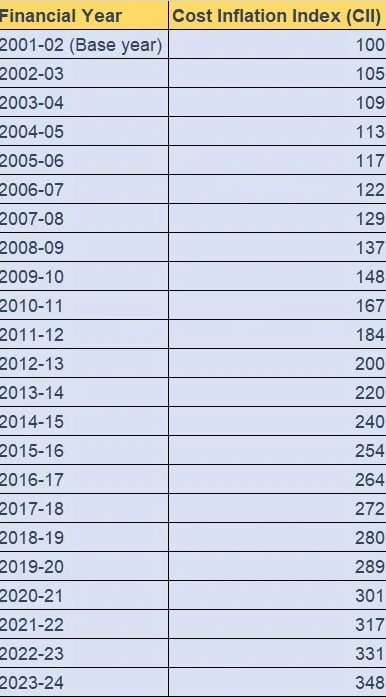

Cost inflation index (CII) is used to adjust the acquisition and improvement costs for inflation over the years. This adjustment helps in arriving at a more accurate capital gain figure.

Cost Inflation Index Table from FY 2001-02 to FY 2023-24 LTCG = Sales - [(Cost of purchase X CII of the year of Sale)/CII of the year of purchase)]

Exemptions and Deductions

The Income Tax Act offers certain exemptions and deductions to reduce the tax burden on capital gains. Some of these include:

Section 54: Exemption on LTCG from the sale of a residential property if the proceeds are invested in purchasing another residential property.

Section 54F: Exemption on LTCG from the sale of any asset (except a residential property) if the gains are invested in purchasing a residential property.

Section 54EC: Exemption on LTCG if the gains are invested in specific bonds within six months of the asset's sale.

Tax Rates on Capital Gains

The tax rates for capital gains differ based on whether they are short-term or long-term.

STCG: Short-term capital gains are added to the taxpayer's total income and taxed at the applicable slab rate.

LTCG: Long-term capital gains from the sale of listed securities and equity-oriented mutual funds are taxed at 10% if the gains exceed ₹1 lakh. For other LTCG, the tax rate is 20%.

Capital Gain Computation for Different Assets

Different types of assets are subject to varying capital gain calculations. Let's explore a few examples:

Real Estate Property

When selling a property, the sale price is reduced by the indexed cost of acquisition and improvement. The resulting gain is then subject to taxation.

Stocks and Equity Mutual Funds

For stocks and equity-oriented mutual funds, LTCG exceeding ₹1 lakh is taxed at 10%. However, gains up to January 31, 2018, are grandfathered, meaning they are exempt from tax.

Navigating Capital Losses

Capital losses can be set off against capital gains to lower the overall tax liability. If the losses cannot be fully set off in the current year, they can be carried forward for up to eight subsequent assessment years.

FAQs

Q: How is the holding period of an asset determined?

A: The holding period is calculated from the date of acquisition to the date of sale.

Q: Are there any assets exempt from capital gains tax?

A: Yes, certain assets such as government bonds and specific agricultural land are exempt from capital gains tax.

Q: Can capital losses from the sale of one asset be adjusted against gains from another asset?

A: No, capital losses can only be set off against capital gains of the same type.

Q: What is the significance of the cost inflation index (CII)? A: CII helps adjust the acquisition and improvement costs of assets to account for inflation over the years.

Q: Is there a difference in taxation for resident and non-resident taxpayers?

A: Yes, non-resident taxpayers might be subject to different tax rates and exemptions.

Q: How can I claim exemptions under Sections 54 and 54F?

A: To claim these exemptions, the taxpayer needs to fulfill certain conditions and invest the gains in eligible assets within the stipulated time.

Conclusion

Navigating the realm of capital gains under the Income Tax Act in India requires a solid understanding of the rules, exemptions, and calculations involved. Whether you're a seasoned investor or a taxpayer looking to make the most of your financial decisions, being well-versed in the intricacies of capital gains is paramount. Remember to consult with tax professionals for personalized advice based on your specific situation.

Services

Audit & Assurance

Financial Advisory

Tax Consultancy

Corporate Compliance

Industries

Consumer goods

Transport

Financial Consultancy

Energy & Technology

Engineering & Constructions